Policy

What you need to know about NYC retirees’ health care fight

A Manhattan judge temporarily blocked the city’s long pursued and controversial plan to switch city retirees to a privatized Medicare Advantage plan.

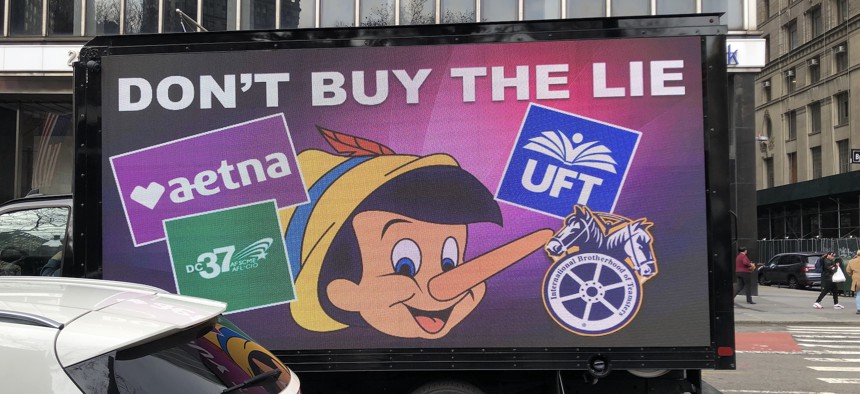

Although Medicare Advantage will still be free, the New York City Organization of Public Service Retirees has raised concerns that retirees will be stuck with a smaller network of providers and larger out-of-pocket costs. Jeff Coltin

New York City can’t switch up retirees’ health care plans just yet. On July 7, Manhattan Supreme Court Justice Lyle Frank temporarily blocked a move by the city to automatically switch more than 250,000 retired New York City employees to a privatized Medicare Advantage insurance plan. The planned switch has received steady pushback from some retirees since it was proposed in an agreement between leaders of the city’s labor unions and former Mayor Bill de Blasio’s administration to find health care savings.

Progress on the planned switch has moved slowly under Mayor Eric Adams as retirees continue to fight it, including in a recent lawsuit. In early March, the city’s Municipal Labor Committee approved a plan for Aetna to provide a Medicare Advantage plan as the only health care option for retirees. After the Daily News reported in late March that retirees fighting the move hoped to utilize an option in the contract that might allow them to keep their traditional Medicare coverage without paying premiums, the Adams administration quickly shot down the prospect, arguing that the option wouldn’t allow the city to realize the $600 million in savings on retiree health care spending that it’s seeking. On March 30, the Adams administration announced that the city had signed a contract with Aetna to provide Medicare Advantage to retirees, with Adams calling it “in the best interests of both our city’s retirees and its taxpayers.” In late May, a group of city retirees sued to block the transition, arguing that it would violate their rights to their existing plans. The latest ruling from Frank hands a preliminary victory to those retirees.

Here’s what you need to know about the drawn out conflict. This post was originally published on January 6, 2023. It was last updated July 11, 2023.

Why is the city proposing this switch?

New York City employees and their dependents have long received health insurance after retirement. When retirees become eligible, they enroll in traditional Medicare, but the city also fully subsidizes a popular supplemental coverage plan provided by EmblemHealth and known as Senior Care.

But New York City and its unions needed to find savings due to rising health care costs. The fund that covers premium costs and other benefits is jointly controlled by the city and unions and is becoming depleted. It’s called the Joint Health Insurance Premium Stabilization Fund. The city and the Municipal Labor Committee, an umbrella organization of the city’s labor unions, reached an agreement in 2018 to find substantial savings in the city’s spending on health care, including $600 million in recurring savings. One option in that agreement, which the city and unions have decided to pursue, was switching retirees to Medicare Advantage. Medicare Advantage is an alternative to traditional Medicare that is provided by private companies that the federal government contracts with. The plans tend to offer lower premiums but can also come with narrower networks and higher out-of-pocket costs, and federal investigators have found the plans often deny necessary care. The city estimated that switching retirees to Medicare Advantage would save $600 million a year thanks to federal subsidies that Medicare Advantage plans receive, with those savings replenishing the city’s depleting fund for premiums and benefits.

Why are some retirees fighting the switch to Medicare Advantage?

Although the switch to Medicare Advantage was agreed upon by the city and union leaders, many city retirees have pushed back against the change. Medicare Advantage will still be free, but the New York City Organization of Public Service Retirees has raised concerns that retirees will be stuck with a smaller network of providers and larger out-of-pocket costs.

The Adams administration has publicly tried to assuage some of those concerns. “We also heard the concerns of retirees and worked to significantly limit the number of procedures subject to prior authorization under this plan,” Adams said in a statement on March 30” But some retirees are not convinced, citing studies into denials of care under the plan.

Are all city retirees going on Medicare Advantage?

That answer depends on the outcome of the retirees’ current lawsuit – and any appeals.

The city initially wanted to offer retirees a choice between going on Medicare Advantage or paying $191 per month to keep their old coverage. The Organization of Public Service Retirees sued before the switch was initially set to go into effect last January to stop the city from making retirees pay to keep their current coverage. In March 2022, a judge ruled in favor of retirees, citing a section of the city’s Administrative Code that requires the city to pay the entire cost of health insurance for employees, retirees and dependents. The ruling, which was upheld on appeal, said that the city could still proceed with the switch to Medicare Advantage but that it couldn’t force retirees to pay to maintain their current coverage if they wanted to opt out. Had they proceeded, it would leave the city and the Municipal Labor Committee in a bind to realize the promised health savings if they had to continue to cover premium costs for the large number of retirees who opt out.

The Adams administration has tried to get around the ruling by amending the Administrative Code. Earlier this year, the administration called on the City Council to pass a bill to change the code, allowing retirees to opt out of Medicare Advantage in favor of their current coverage for a monthly fee of $191. At the request of the mayor, Council Member Carmen De La Rosa, who chairs the Committee on Civil Service, introduced a bill to do so in January, but the proposal was met with swift and fierce pushback from retirees and some council members over the idea of burdening retirees with fees to keep their existing plan. The City Council did not pursue the bill further.

Union leaders and City Hall have said that if the City Council ever agrees to amend the Administrative Code, then they are happy to offer an alternative – the option for retirees to pay $191 per month and remain on their current health insurance. But as of now, the Administrative Code won’t allow that, so retirees will not be able to keep their current plans if the switch goes into effect.

Marianne Pizzitola, president of the NYC Organization of Public Service Retirees, was among those who urged the council to vote down the proposed legislation and called for an alternative to the choice of Medicare Advantage or paying to maintain current coverage. “We are happy to meet with the Adams administration as well as Speaker Adams to outline over $300 million in potential savings without placing an undue burden on hundreds of thousands of the retirees who kept New York City running for decades,” she said at the time.

What’s the latest?

On July 7, Manhattan Supreme Court Justice Lyle Frank granted a preliminary injunction stopping the city from switching retirees to the Aetna Medicare Advantage plan in September. Frank wrote that the retirees would likely find success on the merits of their suit, in which they argued that the switch would force them to accept an inferior plan and that they had been promised the supplemental Medicare coverage they currently receive.

The New York City Organization of Public Service Retirees, a plaintiff in the lawsuit, celebrated the initial victory. “This is now the third time in the last two years that courts have had to step in and stop the City from violating retirees’ healthcare rights,” Pizzitola said in a statement. “We call on the City and the Municipal Labor Committee to end their ruthless and unlawful campaign to deprive retired municipal workers of the healthcare benefits they earned.”

City Hall, meanwhile, expressed disappointment in the decision. “The city’s Medicare Advantage plan, which was negotiated in close partnership with the Municipal Labor Committee, improves upon retirees’ current plans, including offering a lower deductible, a cap on out-of-pocket expenses, and new benefits, like transportation, fitness programs and wellness incentive,” Adams press secretary Jonah Allon told Gothamist.